A Deep Dive into Germany’s Fuel Market with 6 Actionable Insights for Fleet Managers

Rally was built around a simple premise: real savings.

But does the open market win "fuel discounts" and locked prices? To test that, we analyzed 2M+ fuel data points daily, turning pump prices into profit insights.

In this article, we share our original data analysis into fuel price patterns for the German market. But for our customers, we do a lot more, including personalized insights based on the stations they refuel at, driver patterns and access to live fuel price data.

In 30 seconds – What Fleet Managers Need to Know

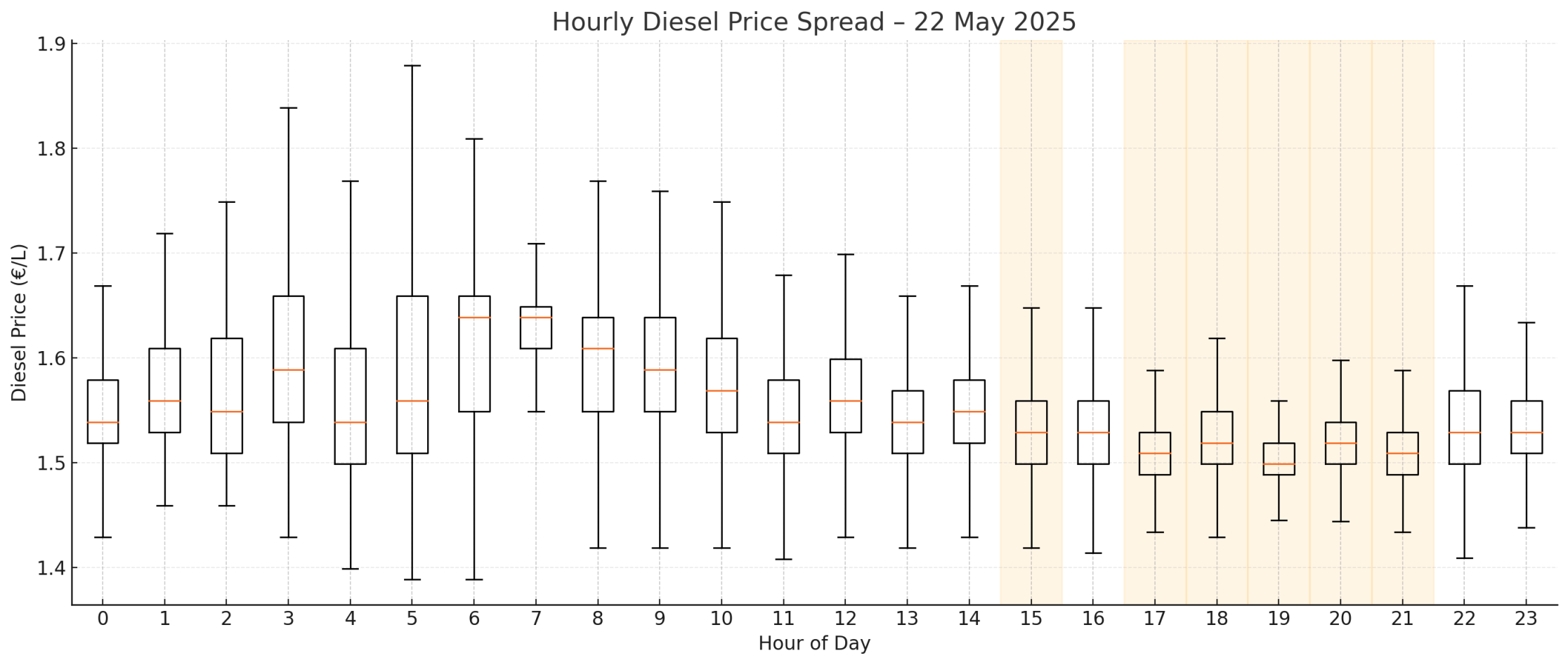

- Evening refueling (17:00–22:00) is reliably cheaper across all fuels.

- Intraday price swings hit 30 ¢/L on average; timing matters.

- Motorway stops still punish you with >30 c/L mark‑ups.

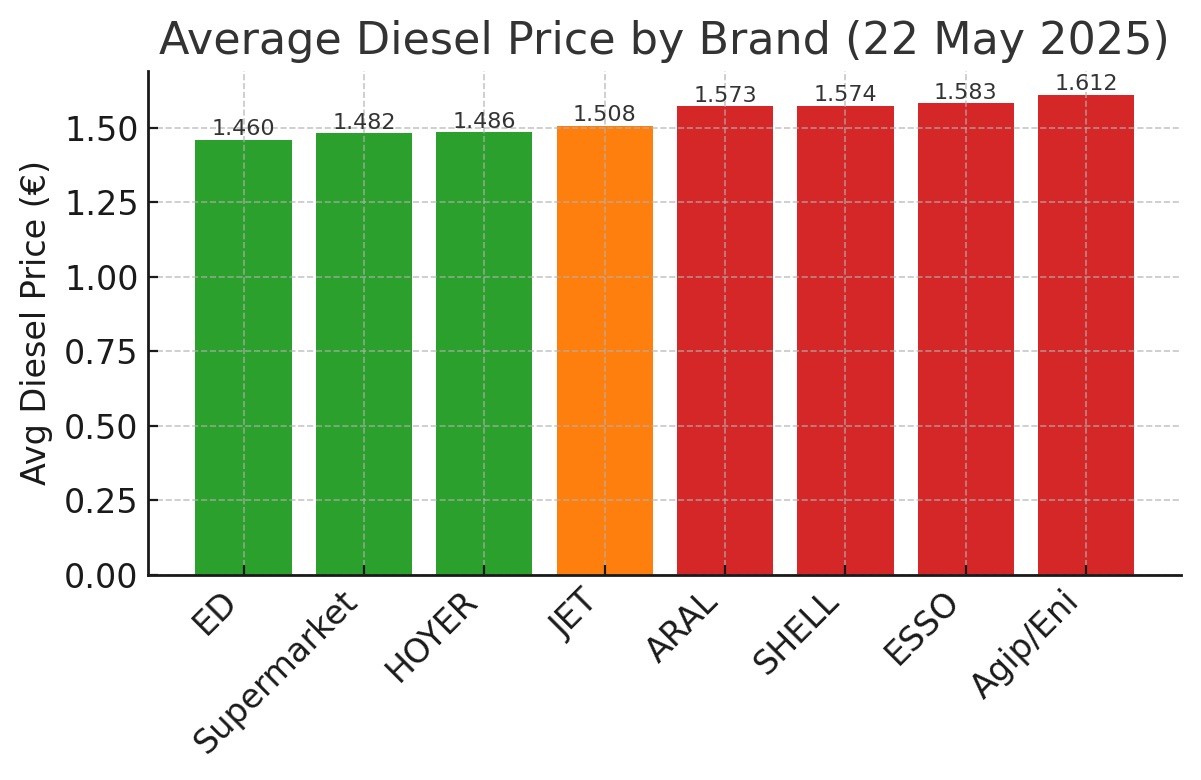

- JET and ED are the cheapest national brands; Shell, Aral, and Agip/Eni are the costliest.

- Less than 1 % of stations are true pricing outliers. There are no silver bullets here.

- A card that works everywhere beats fixed 5 c/L “discount” programmes.

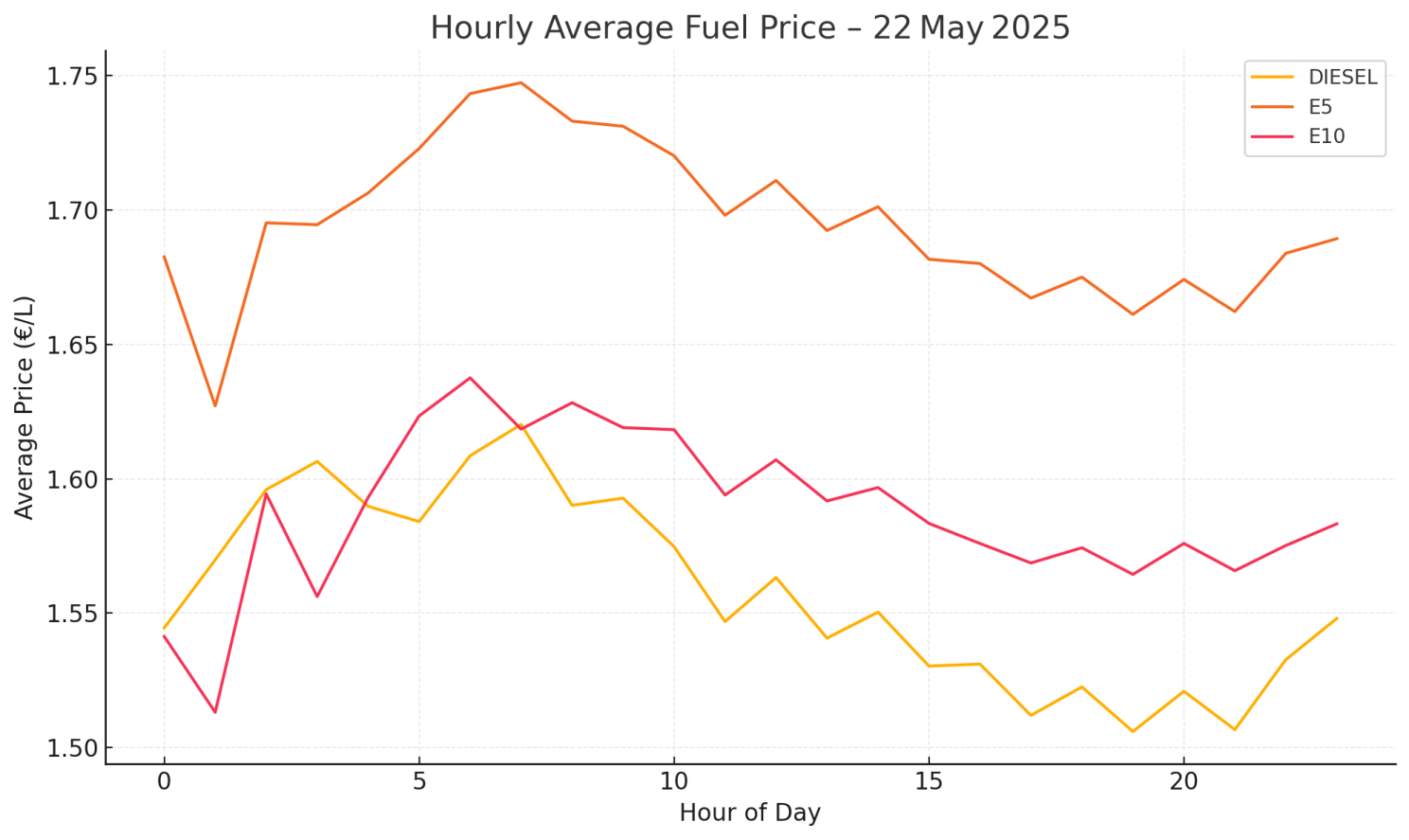

1 - Is there such a thing as a better time of day to refuel? Yes

Across all fuel types, and all stations in Germany, fuel prices are updated every 10 minutes. Our analysis shows that prices are consistently expensive at the beginning of the day.

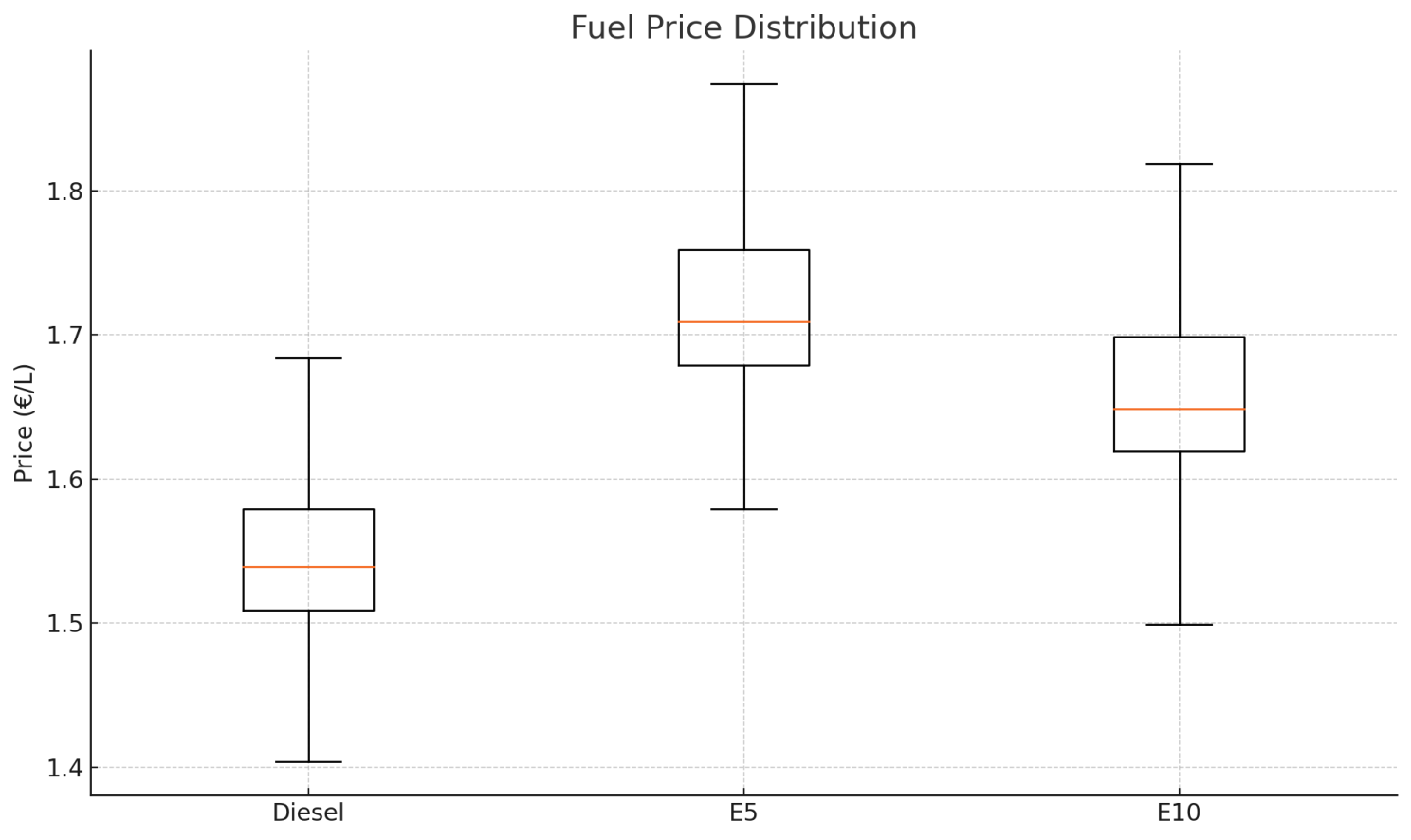

2 - Do fuel prices vary a lot on a given day?

On the days analyzed, diesel prices ranged from €1.419 per liter at the cheapest station to €2.119 per liter at the most expensive (a motorway service) – a difference of 70 cents! Generally, our data shows the fuel price can vary as much as 30 cents on average. This is obviously for all of Germany, but there are also regional effects. What's more interesting is that previous reports stated lower differences only. Outside of this analysis, we see bigger price differences with AdBlue (some customers paying €0.3 while others pay €1.5).

3 - Is there a specific time when fuel prices will be guaranteed to be lower?

A resounding yes. Towards the end of the day, price changes stabilize. 17-22 are guaranteed to give better prices.

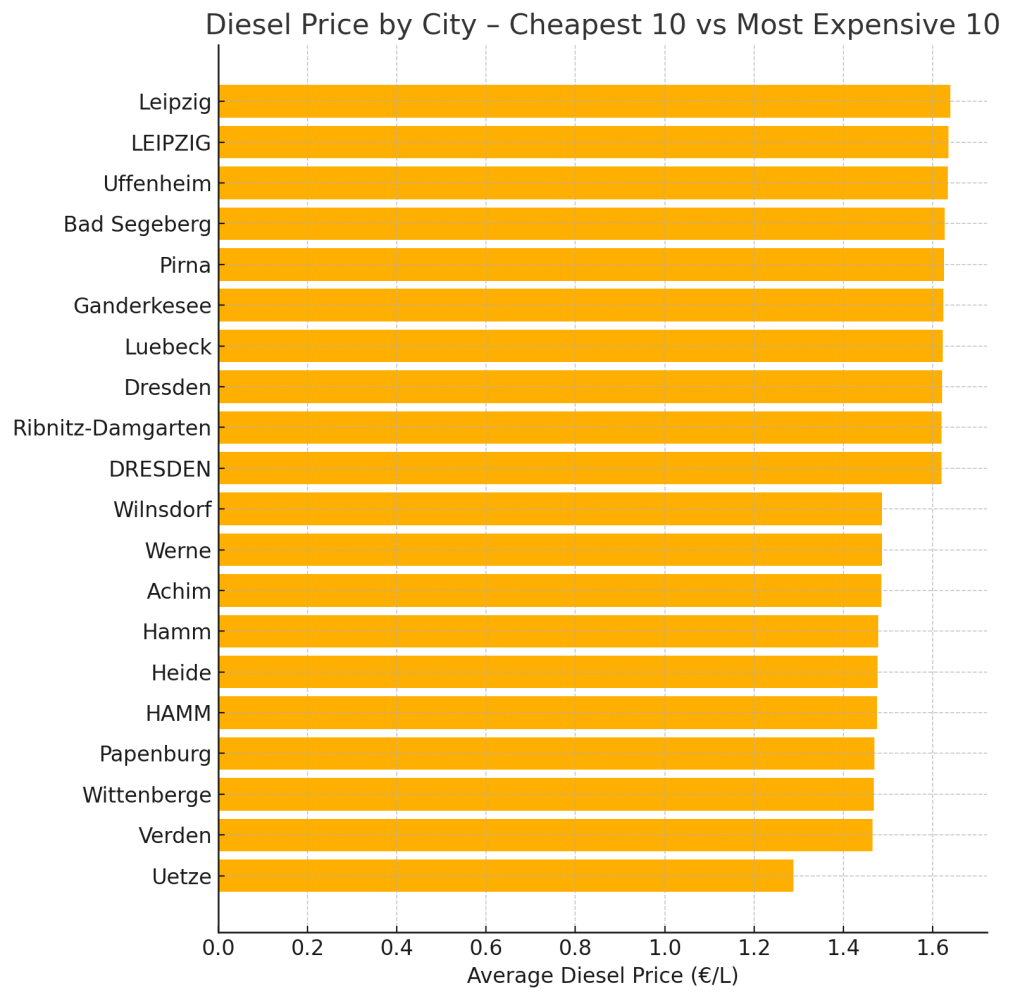

4 - What are the cheapest and most expensive cities in Germany to refuel?

Surprisingly Berlin wasn't in the top 1, but perhaps that's due to stations being in nearby towns and vicinities instead of city centers.

5 - Are there cheaper brands to refuel?

Absolutely, and that's an advantage of the Rally card. Brands like JET and ED have much less stations, but with a card that works everywhere, that's less of a problem.

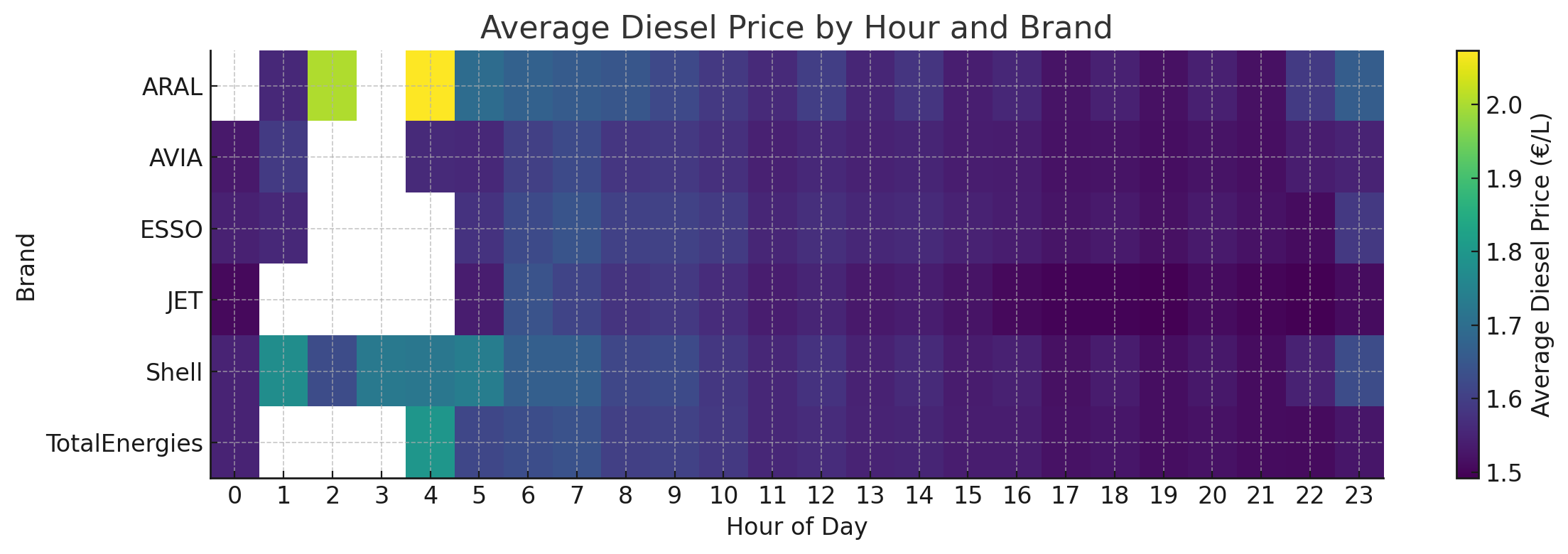

6 - Are there brands that offer lower prices than others at a given time of day?

The usual low-cost suspects are a clear winner here, while others like TotalEnergies show that they try to optimize their costs towards the end of the day to avoid commercial refueling being too cheap.

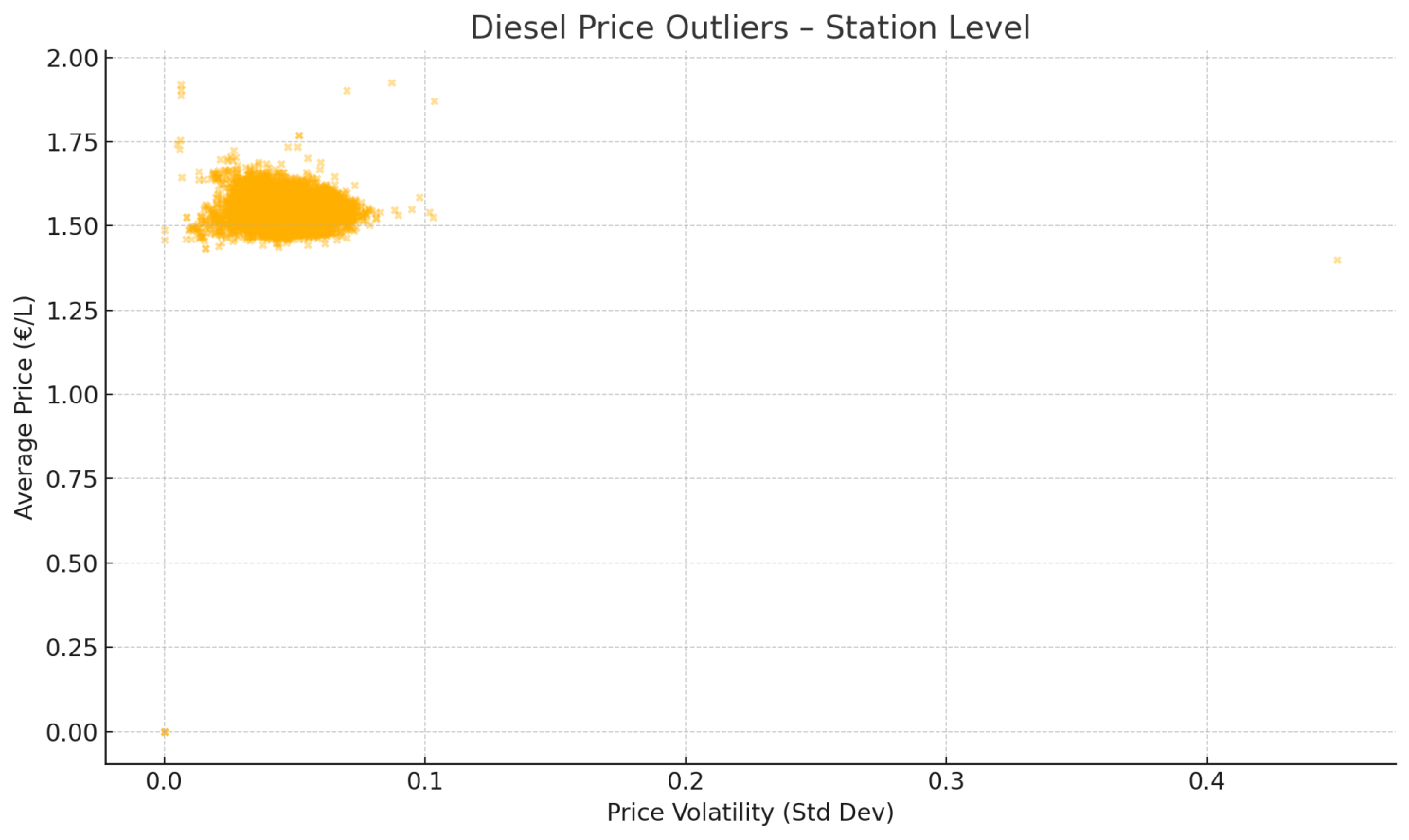

7 - At the station level, are there any outliers?

Yes and no. There are very few outliers in the entire country, likely far-off stations where they don't have leverage. The rest is quite concentrated, and the left chunk of stations (the majority) are probably well-positioned stations in autobahns and other areas where they have leverage.

Conclusion: Are Fleet Discounts Overrated?

Yes – in pure fuel cost terms, fleet card discounts tend to be overrated when compared to open-market purchasing. The data illustrates that the breakeven per-liter advantage of fleet cards (€0.04–0.06) is often overshadowed by the price differences between stations.

- A savvy fleet driver buying on the open market can routinely save as much or more simply by choosing cheaper stations, especially by avoiding high-priced locations. Fixed discounts from premium-brand fuel cards do provide a small benefit, but they rarely guarantee the lowest price.

- In most cases, an open fueling policy (refuel at the station with the lowest real-time price) yields equal or greater monthly savings per liter.

European fleets most often contract one of two pricing models:

- Per-liter discounts – fixed rebates off the posted pump price, typically 2–3 ¢/L from cards like DKV (2 ¢/L on diesel) or Euroshell (up to 3 ¢/L), with volume-tier schemes sometimes reaching 4–6 ¢/L at high monthly volumes.

- Locked-price agreements – you commit to a set number of liters over a period (often several months) at a pre-agreed price; these contracts hedge volatility but usually restrict you to certain networks and minimum volumes.

Neither model fully offsets real-world price spreads. Our data from the German market shows local intraday and regional price gaps commonly exceed 20 ¢/L within the same town, and motorway stations average 25 ¢/L more than nearby off-highway pumps. A 4–6 ¢/L rebate or a locked price that tracks market averages therefore covers only a sliver of these spreads. By contrast, open-market fueling – letting drivers fill up at the cheapest available station in real time – routinely undercuts both contract types on a per-liter basis.

Thanks to these insights and to our free-market approach, one of our customers saved 45k € / year on fuel, and we’re only getting started. Fuel is usually the biggest line-item after people, and we see a lot more opportunities that only a modern fleet product can improve.

Rally (YC W25) helps European fleets with real money and time savings. We’re bringing fleet payments into the modern era with full visibility, total control, and zero fluff.

- 🌍 Live in 24 countries

- ⛽ Accepted at 1M+ fuel stations

- ⚡ Built for fleets including EVs