Download the template first, read the rules after: our free declaratieformulier is a ready-to-use Excel expense claim form built for Dutch payroll and bookkeeping practice in 2026. It splits VAT per line, categorises spend with dropdowns, and calculates mileage at the new €0.25 per kilometre — the rate that applies retroactively from 1 January 2026 and that most older forms still show as €0.23.

Download the free declaratieformulier (Excel) — no e-mail address required.

The form is in Dutch, because that is what your employees, approvers, and accountant work with. Below is everything the form has to get right — and what the Belastingdienst expects when it looks at one.

What the Template Includes

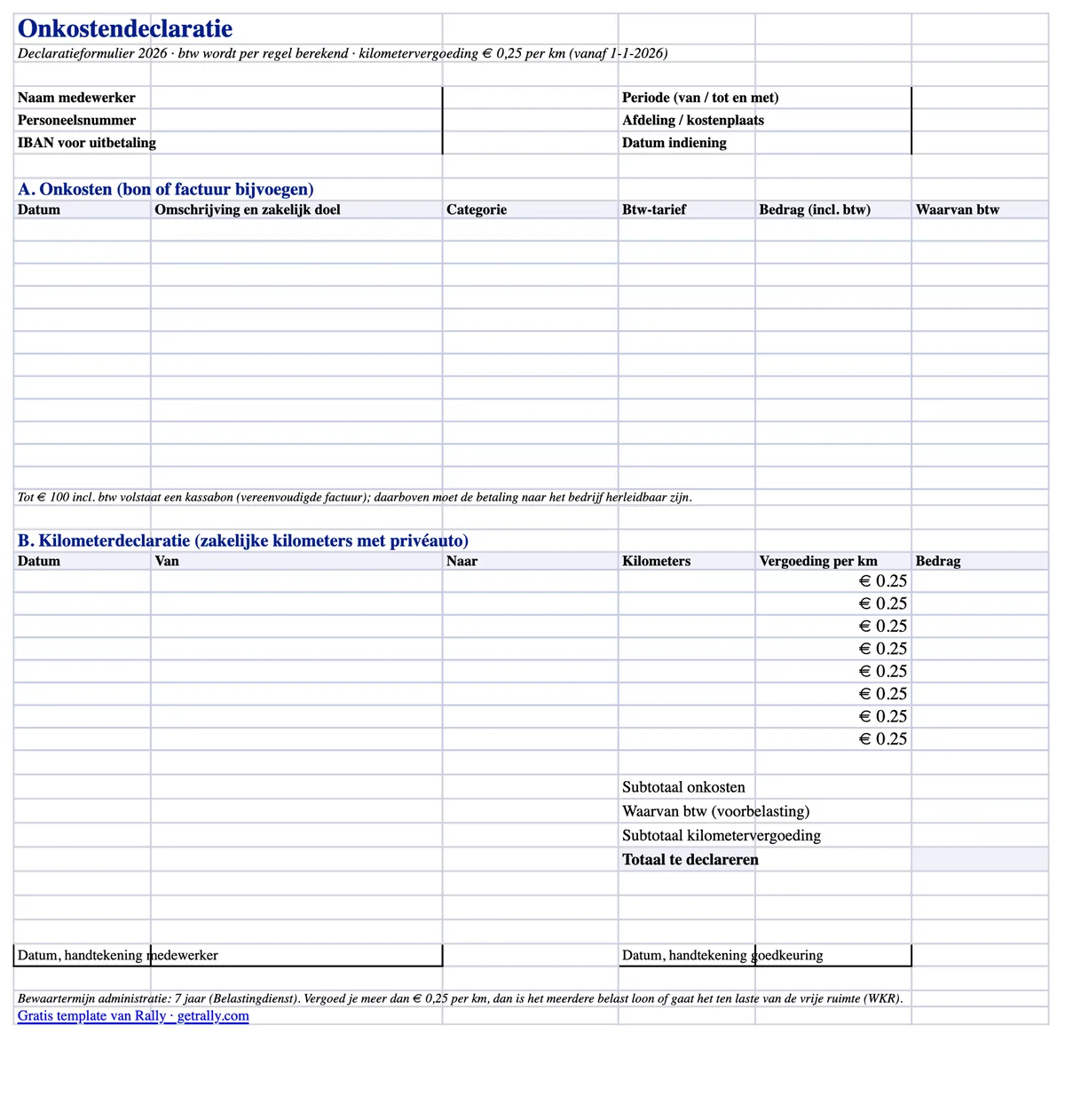

The Excel file is a single A4-printable sheet with two claim sections and automatic totals:

- Expense lines with a VAT split. Each line has the date, a description with the business purpose, a category dropdown (fuel, EV charging, parking, tolls, meals, overnight stays, materials, other), a VAT-rate dropdown (21% / 9% / 0%), and the gross amount. The VAT portion is calculated automatically per line, so your bookkeeper can post the voorbelasting without a calculator.

- A mileage section (kilometerdeclaratie). Date, from/to, and business kilometres — multiplied by an editable rate pre-filled at €0.25, the 2026 tax-free maximum.

- Automatic totals. Subtotal of expenses, total reclaimable VAT, mileage subtotal, and the grand total to reimburse.

- Header and signature blocks. Employee name, personnel number, department or cost centre, claim period, IBAN, and signature lines for the employee and the approver.

It works in Excel, LibreOffice, and Google Sheets, and prints cleanly if your process is still paper-based.

What a Declaratieformulier Must Contain

Dutch law does not prescribe a fixed expense-claim form, but the administratieplicht does require that your records show what was reimbursed, to whom, and why it was a business cost. In practice a claim needs:

- Who claims: name, personnel number, department or cost centre.

- What and why: date, description, and the business purpose of each expense. "Lunch" is not a business purpose; "lunch with customer X during site visit" is.

- How much: the gross amount and the VAT per line, matching the receipt.

- Proof: a receipt or invoice attached for every line.

- Approval: the employee's signature (or digital submission) and the approver's sign-off, with dates.

Miss the business purpose or the receipt, and a reimbursement risks being reclassified as taxable wages during a payroll audit — with the employer picking up the loonheffing.

Receipts and VAT: When a Kassabon Is Enough

The rule that trips up most claims is the invoice requirement for VAT recovery:

- Up to €100 including VAT, a vereenvoudigde factuur is sufficient — and an ordinary till receipt usually qualifies. It must show the date, the supplier's name and address, the nature of the goods or services, and the VAT amount (or the data to compute it). The employee's or company's name does not need to be on it.

- Above €100, the buyer must be identifiable. The company's details on the invoice are the clean solution; for fuel and similar road spend, the Belastingdienst accepts that the payment itself is traceable to the business — paid with a company card or fuel card rather than the employee's private one.

VAT on a compliant receipt is deductible as voorbelasting to the extent the company makes VAT-taxed supplies. VAT on a missing or deficient receipt is simply lost — which is why the template has a column for it on every line.

Mileage in 2026: €0.25 per Kilometre, Retroactively

The tax-free mileage allowance (onbelaste kilometervergoeding) rose from €0.23 to €0.25 per business kilometre in 2026. The increase was approved mid-year by policy decision, ahead of the Belastingplan 2027, and applies retroactively from 1 January 2026.

Practical consequences for your claims process:

- New claims: reimburse at €0.25/km tax-free. The template's rate column is pre-filled accordingly (and editable if your policy pays less).

- Already-paid 2026 claims at €0.23: the missing €0.02/km may be paid out tax-free with a later salary run.

- Employers who paid more than €0.23 and taxed the excess: earlier payroll returns can be corrected per the Handboek Loonheffingen procedure.

Note the boundary: €0.25/km is the tax-free maximum as a targeted exemption. Anything above it is taxable wages — or consumes WKR budget if designated as eindheffingsloon.

Where the WKR Fits In

Every reimbursement on a declaratieformulier lands in one of three tax buckets:

- Intermediaire kosten — the employee paid for something that belongs to the employer (materials for a job, fuel for a company van). No wage tax dimension at all.

- Gerichte vrijstellingen — targeted exemptions such as business mileage up to €0.25/km, public transport, and meals during business trips. Tax-free, without touching the WKR budget.

- Everything else — tax-free only within the WKR vrije ruimte: in 2026, 2.00% of the first €400,000 of the fiscal wage bill plus 1.18% above it. Exceed it, and the employer pays an 80% eindheffing on the excess.

A well-categorised claim form is your first line of defence here: if fuel for the company van, mileage, and a team dinner are all mushed into one "expenses" line, your WKR administration inherits the mess.

Common Mistakes on Expense Claims

The errors payroll auditors actually find:

- No business purpose recorded. The single most common defect — and the easiest to fix with a mandatory description field.

- VAT reclaimed without a qualifying receipt, or from a receipt over €100 that identifies nobody.

- The old €0.23 rate hard-coded in forms and policies after the 2026 increase — money left on the table for every employee.

- Private kilometres claimed as business — commuting is not a business trip, though it may qualify for its own reiskostenvergoeding arrangements.

- Claims submitted months late, after the receipt has faded or disappeared, then reimbursed anyway without proof.

- Receipts stored nowhere. The bewaarplicht is seven years; a shoebox is technically compliant but practically hopeless. Scans are fine if they faithfully reproduce the original.

When the Form Itself Is the Problem

A template fixes the format of expense claims. It does not fix the workflow: employees fronting company costs from private money, photographing crumpled receipts weeks later, finance chasing missing bonnetjes, and VAT quietly leaking on every non-compliant line.

That workflow is worth eliminating rather than formatting. With company cards for employees, the payment and the receipt are captured at the moment of purchase — drivers and field staff snap the bonnetje via WhatsApp, the transaction is categorised automatically, and finance gets export-ready records instead of a stack of forms. For teams on the road it covers the whole spend surface in one card: fuel, EV charging, parking, tolls, and the materials run. The declaratieformulier then survives only for the genuine exception — the private-car kilometre claim — instead of being the default process. Our guide to expense cards for employees walks through what that transition looks like.

Sources

This article is general information, not tax advice. Rates and thresholds are set by the Dutch government and can change; verify specifics for your situation with your accountant or belastingadviseur.